In the world of estate planning, wills and trusts often take center stage. They’re kind of like siblings (without all the fighting). Both are legal tools that transfer your stuff to those you love.

The main difference is that one takes over while you’re still alive and the other goes into effect after you die.

There are a few more important distinctions you should know about. Let’s go over each one, starting with the basics so you can decide what’s best for you.

What Is a Will?

A will is a legal document that explains what you want to happen when you die—and puts it all in writing. It outlines things like who you want to get your stuff, your money, and guardianship of your kids or pets.

There are many different types of wills. But for most people, a simple will is enough. In fact, for 95% of people, a will is all you need to establish a rock-solid estate plan—one that protects your family if something ever happens to you (and it will, eventually at least).

If you have less than $1 million in assets, you can just stop right here and get yourself a will. (Unless you really want to learn about living trusts as a kind of hobby. More power to you!)

If you think you might be in that 5% of people who need more than a will, keep reading.

What Is a Trust?

Trusts come in lots of different forms—close to a dozen, actually. So let’s focus on the most common ones and what they do.

Living Trust

A living trust lets you transfer your assets to loved ones quickly and easily. It’s “living” because it’s in effect while you’re alive, as opposed to a will, which only kicks into gear after you’re gone. You can put things like bank or savings accounts, cars, real estate, art, jewelry and even intellectual property (like your novel manuscript) in a living trust. But even though those assets are named inside your trust, other people can’t access them until after your death.

Revocable and Irrevocable Trusts

A revocable trust just means you can change the terms of the trust. How about an irrevocable trust? Yep, you guessed it. You can’t change the terms. For example, in an irrevocable trust, once you name the beneficiaries for your property, the names of those beneficiaries are set in stone and can’t be changed.

You can make most other kinds of trusts revocable or irrevocable. Revocable trusts are the most common, but even making changes to a revocable trust takes a lot of paperwork. Fun fact: Revocable trusts magically transform into irrevocable trusts after your death.

Charitable Trust

As the name suggests, a charitable trust is used to give away part of your estate to a charity. You can create a charitable lead trust (CLT) or a charitable remainder trust (CRT). The CLT is simple: You designate particular assets to go toward your favorite charity (like Agatha’s Donkey Shelter, for example). With a CRT, you put certain assets into the trust that you or your beneficiaries will get income from, and the rest of your assets go to one or more charities.

Testamentary Trust

A testamentary trust is one you create using a will. So in your will, you basically say, “When I die, this and this will be placed into a trust for this person.” The kind of trust (like charitable or special needs) you create is up to you.

Spendthrift Trust

Some people just don’t know how to handle money. If you’re looking at your loved ones and thinking, Yep—that’s them, a spendthrift trust might be a good option for you. This kind of trust allows you to control when and how your beneficiaries get your stuff.

Special Needs Trust

Using this trust, you can make sure any dependents with special needs will be supported and cared for after you’re gone.

Life Insurance Trust

Life insurance death benefits aren’t usually taxable. But if you’re super wealthy and your death benefit will cause your estate to be worth more than $12.92 million for a single person, those benefits will become subject to the federal estate tax.

Save 10% on your will with the RAMSEY10 promo code

So, a life insurance trust includes your insurance policy and can protect your death benefit from estate taxes when you pass away.

These are just some of the different types of trusts. They can get even more specialized depending on your needs. As you can see, trusts tend to be geared toward people with complex estates.

Don't Know Where to Start With a Will?

Download our will worksheet to get started.

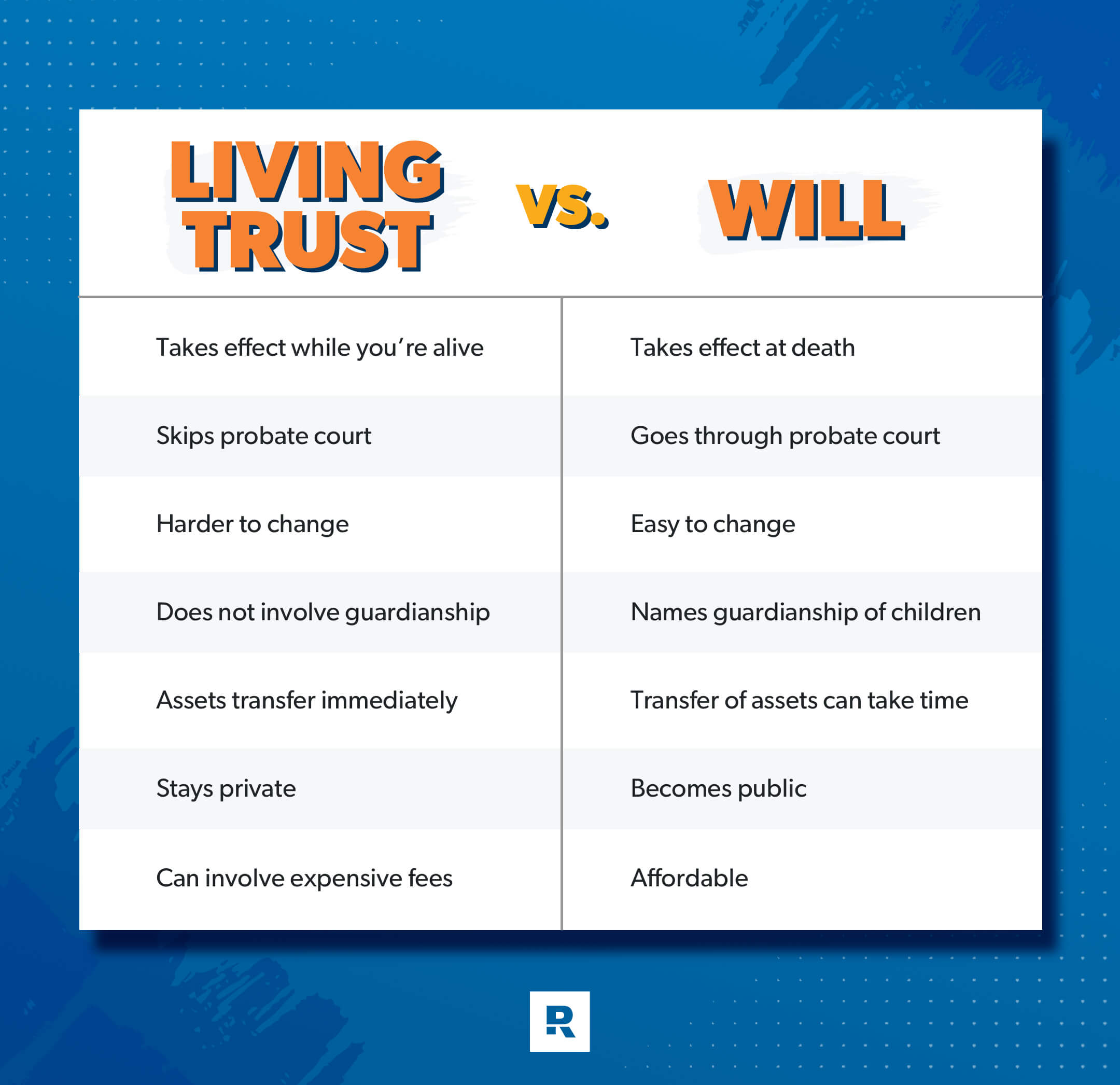

What’s Covered in a Will vs. Trust?

So, now that we’ve gone over what wills and trusts are, what sets them apart?

One of the most important differences between wills and trusts is the ability to name a guardian for your minor children. You can name a legal guardian in your will, but you can’t in a trust. So, even if you have a trust, you still need a will to make sure your kids are taken care of after you die.

Another important distinction between the two is that, unlike a will, a trust lets you skip probate court. Probate court cases can be expensive and drag on forever. So, skipping them is a big deal. If your estate gets mixed up in probate court because a loved one challenges the will, it could mean your family has to spend the next year heading to court while grieving. Not fun.

But remember, if your will is clear and you don’t have a huge estate (or if you have a lot of debt—yuck), probate won’t be a huge hassle. And you probably don’t need a trust.

And while we’re on the subject of probate court, let’s talk about some family stuff.

There’s a little crazy in every family. You know who they are in your family (and if you don’t, it might be you). But some families deal with more than their fair share.

Wills are best for families that struggle with trust issues (not the kind you’re thinking of) and tension between family members because probate court can resolve those issues. On the other hand, families who can handle healthy conflict and have a lot of confidence in each other are better off with a trust since they don’t need a probate court to babysit them.

And if you’re wondering if you can have both a trust and a will, the answer is yes. In fact, most people who have a trust have a will too.

Will vs. Trust: How Much Does It Cost to Set Up?

In general, trusts can be more complicated and expensive to set up and maintain than wills. The exact cost depends on the type of trust, your location, and how complex the document is.

But remember, even though trusts might be more expensive up front, they could save your family money in the long run by avoiding probate court.

Wills, on the other hand, are generally easier to create and cost less to carry out. So, they’re cheaper up front than a trust. Again though, the ultimate cost of a will depends on how simple or complicated it is.

Will vs. Trust: Which Is Best?

Now comes the big question: Should you get a trust, a will or (drumroll, please) . . . both? It really boils down to personal choice.

First, take a big-picture look at your needs and your overall life circumstances.

- Just a will: A will is the best option if you’re like the average person with a couple of kids and a house. You won’t need a lawyer unless there’s something really complicated about your situation. You can set up a will in just a few minutes yourself online. That means no more excuses. Get a will!

- Just a trust: A trust might be better if you’re older, your kids are grown, and your estate is worth at least $1 million. This way, you can avoid probate in a way that wills don’t allow.

- Both a will and a living trust: You might need both if you have a large estate and dependents. (Remember, the will fills in that guardianship gap.) And if you do get both, don’t worry about them bumping into each other. They’re separate legal instruments and there usually aren’t any conflicts between them (unlike siblings). If there is a legitimate conflict, the trust overrides the will.

Here's a simple chart that outlines the pros and cons.

So, let’s wrap it all up. The main difference between a will and a trust is that almost everyone needs a will but most people don’t need a trust. Trusts might be more than you need for your situation, but they can also be a great tool if you have a larger estate.

If you’re in the 95% of people who don’t need a trust, just get yourself a will. Don’t put it off—you’ll feel so much better knowing your stuff will go to the right people and your family will be looked after for many years to come.

Next Steps

- If you need a will, take some time to figure out what to include in your will. You also need to decide who gets what and who will be responsible for making sure your wishes are carried out, among other things.

- Grab The Complete Guide to Estate Planning, which will help you understand everything you need to know about estate planning in a simple, straightforward way.

- RamseyTrusted provider Mama Bear Legal Forms makes it super easy to get your will done in a matter of minutes. You can see their packages and pricing options below.

Complete Last Will & Testament Package for One Person

Includes:

- Last Will & Testament

- Health Power of Attorney

- Finance Power of Attorney

Complete Last Will & Testament Package for Married Couples

Includes:

- Two Last Will & Testaments

- Two Health Powers of Attorney

- Two Finance Powers of Attorney

Interested in learning more about estate planning?

Sign up to receive helpful guidance and tools.

Interested in learning more about estate planning?

Sign up to receive helpful guidance and tools.

Frequently Asked Questions

-

Which is better: a trust or a will?

-

It depends on the size of your estate. If your estate is large and complex, a trust could be your best bet. But if your estate is smaller and fairly simple, a will is likely the best option. If you have dependents, you definitely want a will—even if you get a trust too.

-

Are trust assets left to a beneficiary part of your taxable estate?

-

It hinges on how the beneficiary receives distributions (payouts). If the money your beneficiary gets is from the principal (the money or assets you put in originally), then it won’t be taxed. But if your beneficiary is getting payouts from interest earned on the principal, then they’ll owe taxes on that.

-

Does transferring property to a trust protect it from creditors?

-

Probably not. There are a few trusts called asset protection trusts that aim to do that, but they don’t have a 100% success rate. Most trusts aren’t a good bet for protecting property from people you owe money to.

A revocable trust offers no protection because you still own the property, while an irrevocable trust can offer some shelter because technically you no longer own what’s inside. But your best option is paying off your debt. Then you can know for sure your loved ones will get what you want them to have.

-

What assets cannot be placed in a trust?

-

There are a couple things you can’t put in a trust:

- Foreign assets or property

- Retirement accounts and Health Savings Accounts (You can name the trust as the beneficiary on these accounts to fix this problem, though.)

- Cash (But you can put cash in a bank account and name your trust as the beneficiary.)

Did you find this article helpful? Share it!

About the author

Ramsey