So you’re looking to buy a house—congratulations! If you’re not buying with cash, you’re probably also looking for a mortgage and want to get the best rate possible. Who wouldn’t?

Traditionally, the 30-year fixed-rate mortgage is one of the most popular options out there. Most folks you know probably have one. Your parents probably had one. Your dog might have one. But is it really your best bet? Thirty years is a long time, and you want to be sure you’re making the best decision possible!

What exactly is a 30-year fixed-rate mortgage, and what are the pros and cons of taking one out? Let’s find out!

What Is a 30-Year Mortgage?

A 30-year fixed-rate mortgage is basically a home loan that gives you 30 years to pay back the money you borrowed at an interest rate that won’t change. It sounds simple enough. There’s a bit more to it, though.

Let’s say you want to buy a $200,000 house. If you use our mortgage calculator to compare the 15- and 30-year mortgage options, the 30-year mortgage will appear to be cheaper, but that’s only if you’re looking at the lower monthly payment.

Be warned. It might seem like you’re getting a better deal with the cheaper payment (and longer pay period), but in exchange, your lender will slap a higher interest rate on your loan. The rate for a 30-year mortgage is typically .5–.75% higher than the rate for a 15-year mortgage.

So while you’d pay less per month with a 30-year term, you’d be saddled with a higher interest rate. And do you know what a higher interest rate over a longer term means? It means you’re about to waste a boatload of money in interest (as you’ll see when we dig into the numbers below).

How Does a 30-Year Fixed-Rate Mortgage Work?

First, it’s a fixed-rate mortgage, meaning your interest rate stays the same for the life of the loan. For example, a 30-year mortgage with a fixed rate of 4.5% would stay at that rate for the entire 30 years—despite changes in real estate trends.

Get the right mortgage from a trusted lender.

Whether you’re buying or refinancing, you can trust Churchill Mortgage to help you choose the best mortgage with a locked-in rate.

If your interest rate stays the same, so will your monthly payment—which makes a fixed-rate mortgage your best option. If you got a mortgage with one of those rip-off adjustable rates, your interest would yo-yo each year based on market trends—which means your monthly payment could go up or down (let’s be real—up).

To fully understand how a fixed-rate mortgage works, let’s break it down into three parts: interest, principal and amortization.

- Interest: Lenders are interested in letting you borrow their money because they make a chunk of money in return for what they loan you, called interest. With a 30-year mortgage term, your lender gets to collect 30 years’ worth of interest (if you keep the loan for that long). The amount of interest you pay is also determined by the interest rate (a percent of your remaining loan balance). The higher the interest rate, the higher your interest payment—and overall cost of your loan.

- Principal: Principal represents the original amount of money you borrow from your lender to buy your home. If you buy a $200,000 home with a 20% down payment ($40,000) and take out a loan for the rest, your principal balance would be $160,000.

- Amortization: Amortization is a fancy financial term used to describe the process of paying off a mortgage—or putting your debt to death. An amortization table shows you how long your mortgage will last and how much you’ll pay in principal and interest per month or year. Our mortgage payoff calculator goes a step further and shows you how extra or more frequent payments can reduce the amount of time you’re in debt. What it doesn’t show you is the dance moves you can do as you pay off the debt—those will just come naturally.

As you make monthly payments, most of your money will go toward interest and principal. The rest goes toward property taxes, homeowner’s insurance, and—if applicable—homeowner’s association (HOA) dues and private mortgage insurance (PMI).

Dave Ramsey recommends one mortgage company. This one!

Let’s use our mortgage calculator to see how a typical monthly payment works for a 30-year fixed-rate mortgage set at an interest rate of 4.5%. Suppose you buy a $200,000 home with a 20% down payment (to avoid PMI). With no HOA fee required, your monthly payment would be $1,065.

| 30-Year Fixed-Rate Mortgage Expenses | Monthly Payment Amount |

| Principal and Interest | $811 |

| Property Taxes | $183 |

| Homeowner’s Insurance | $71 |

| Total Monthly Payment | $1,065 |

There’s something else you should know about the monthly payment of a 30-year term: You’ll start off paying more of the interest than the principal until about halfway through the life of the loan. Then you’ll swap.

Why, you ask? It’s because the interest amount is based on the outstanding loan balance, which is reduced with each principal payment. As your loan balance goes down, you’ll be charged a smaller amount of interest each month.

But this doesn’t affect the size of the monthly payment, which stays the same for the life of the loan. Using our example, check out the amortization table below for a snapshot of this.

| Year | Month | Interest | Principal | Payment | Loan Balance |

| 1 | 1 | $600 | $211 | $811 | $159,789 |

| 15 | 169 | $416 | $395 | $811 | $110,419 |

| 30 | 360 | $6 | $805 | $811 | $0 |

Look at how the combined interest and principal amount ($811) stays the same for the entire 30 years, while the amount that goes toward interest goes down and principal goes up, until the final payment. With all these ups and downs, paying off a mortgage can feel like riding a roller coaster—the longer you stay on, the sicker you’ll feel.

What Are the Pros and Cons of a 30-Year Fixed-Rate Mortgage?

How can you tell if a 30-year fixed-rate mortgage is right for you? Compare the pros and cons.

- Pros: You have more time to pay back your loan, and your monthly payment is cheaper—compared to a 15-year term for the same loan amount. Plus, the fixed interest rate protects you from the possibility of rising rates that could send your monthly payments through the roof.

- Cons: You’re charged a relatively high interest rate over 30 years, which means you pay an unbelievable amount of interest compared to a 15-year term.

30-Year Term vs. 15-Year Term

A 15-year mortgage is OK (buying a house with cash is what we’ll always recommend). But a 30-year mortgage? Come on. You’re overcooking our grits.

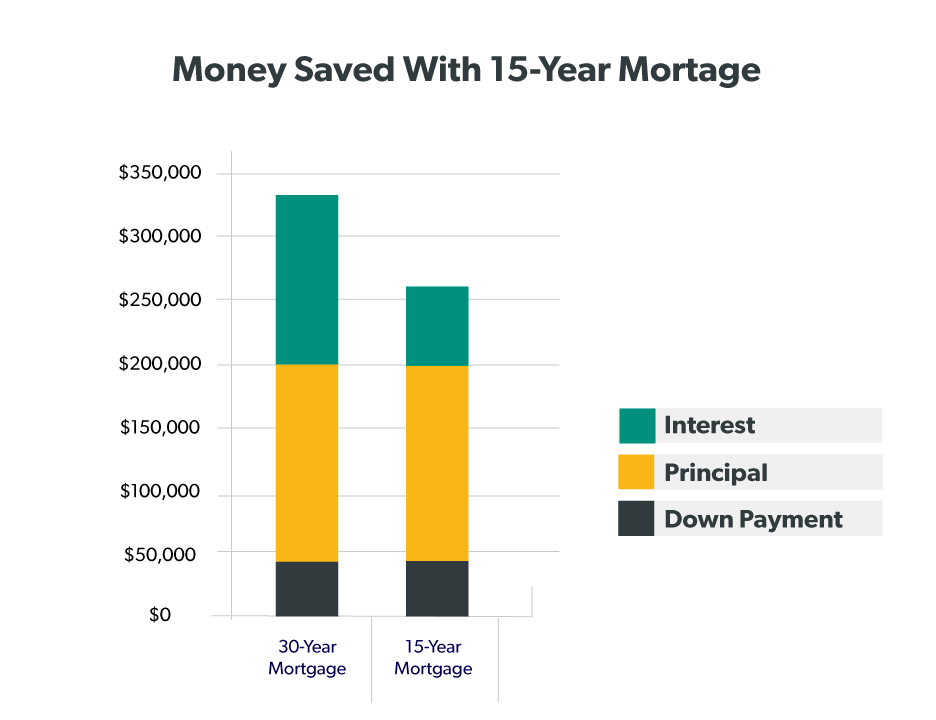

To get a better idea of why 30-year mortgages get on our nerves, let’s compare a 30-year to a 15-year fixed-rate mortgage. Both have fixed interest rates, so the only difference between them is how much interest you pay.

| $200,000 House, 20% Down Payment, Fixed-Rate, Conventional Loan | 30-Year Mortgage | 15-Year Mortgage |

| Interest Rate | 4.5% | 4% |

| Monthly Payment | $811 | $1,184 |

| First Payment | $600 toward interest, $211 toward principal | $533 toward interest, $650 toward principal |

| Total Interest | $132,000 | $54,000 |

Difference: $78,000

A 15-year fixed-rate conventional loan saves you over $78,000! $78,000! Can you imagine the return you’d get on that if you invested it in a Roth IRA or mutual fund.

The Problem With the 30-Year Term

So here’s the big question: After looking at the math, why would anyone choose the 30-year mortgage over the 15-year?

Well, when you think about it, we do a lot of things that don’t make sense.

We say heads up when we mean heads down. We call them chicken fingers, but chickens don’t have fingers. We put pizzas in square boxes even though they’re round. And people who want financial freedom take out 30-year mortgages. Okay, okay, maybe it’s a stretch to compare 30-year mortgages to pizza boxes and chicken fingers. But seriously, contrary to what many people think, the 30-year mortgage is not a smart financial move in the long run.

Most people would probably say, "Look, I just want a cheaper monthly payment. I’m not actually going to stay in the house for 30 years."

The problem with this way of thinking is that it keeps people in debt longer. For example, if you sold the house before the 30-year term was up, you’d have to use a portion of what you earned from the sale to pay off the loan—which means you’d likely take out another loan to buy your next house. Talk about stealing your wealth!

Get a Smart Mortgage

The problem with a 30-year fixed-rate mortgage is that you waste too much money on interest and stay in debt way too long. But go with the 15-year loan, and you’ll save thousands of dollars and pay off your house faster, paving a much smoother path to your other financial goals.

If you like the sound of that, shop smarter with our friends at Churchill Mortgage. Churchill Mortgage will make you their biggest priority. They’re one of the most competent and friendly mortgage lenders out there, and they’ll do everything they can to help you avoid common mortgage traps and save money. Get in touch with a loan specialist at Churchill Mortgage today!

Did you find this article helpful? Share it!

About the author

Ramsey